Jean-Jacques David, The Death of Marat (1793)

Some say the world will end in fire,

Some say in ice.

From what I've tasted of desire

I hold with those who favor fire.

-- Robert Frost, Fire and Ice (1920)

I think most of us are like Robert Frost. I know I am. When I think about how bad things might happen, how our world might end, I tend to imagine it in a series of mighty events like market crashes that explode like bombs and result in a blaze of destruction. That's the romantic in me and Frost, imagining that we perish in fiery excitement.

I suspect, though, that the far more common end is that we die in the bathtub.

Certainly that's what stagflation is, economic death in the bathtub. Economic death by slow, ignominious ice rather than quick, heroic fire. It's not a crushing recession where everyone loses their jobs and a great wailing erupts across the land. It's a long, gray slog where meager real growth feels like death, but you keep up appearances as best you can. Stagflation is a long gray slog where every day you feel more and more stretched ... attenuated ... because nothing is getting cheaper and every now and then you'll be hit with a new price or an unexpected bill that literally takes your breath away. You can manage it. For now. But damn. Stagflation is a long gray slog where you read about people in the news making lots of money or riding some big financial win, all smiles, but in your own financial life and the financial lives of everyone you know the smiles are increasingly wan and forced. Everyone you know is bleeding. Not yet bleeding out. But damn.

Sound familiar?

A big part of my job, and probably my favorite part of the job, is that I get to talk with a lot of people about money. Not money in the aggregate or the generic, and not money in the sense of this stock or that stock, but about their real-life money or about other people's real-life money that they manage or advise. I get to talk with people inside the US and outside the US. I get to talk with people of modest means and with crazy rich people. I get to talk about what they're doing in the real world and what they're doing in the market world. Usually there's a fair amount of difference in what people are doing, even when everyone is nervous about the future. Not today. Not for the past 2 months or so.

Nothing has changed in people's consumption behaviors. Nothing. Everyone is doing everything that they did before. Maybe a little more nervously and maybe a little more on credit, but no one has changed the way they live their lives. The one exception to this is that non-US people are no longer consuming US travel. They're still consuming US education for their kids, but they've cut back on travel to the US in a really major way.

Everything has changed in people's risk-taking behaviors. Everything. The non-US people are bringing their money back home, wherever home is. They want to eliminate their risk exposure to the US, period. The US people are doing nothing in a profound way, by which I mean they are of course eliminating their risk-on behaviors like buying a new house or expanding their company or bankrolling nephew Gary's start-up, but they are also NOT doing the typical risk-off behaviors like selling their stocks and going to cash or slashing the price on that rental house that's been on the market waaay too long or telling little Johnny or Jenny that $100k for another year of 'higher education' at [[checks notes]] the University of Miami is just not in the cards.

I talk with so many people who are frozen in place, for whom 'risk' is less and less a meaningful concept. They're extremely unsure about the future, so they don't want to risk investing in anything new. But they also don't trust the traditional safe havens like Treasuries or (for the more monied crowd) the yen, so they don't want to risk selling anything old. They're domestic US investors, so a falling dollar doesn't hurt them like it does a non-US investor with US assets, and there's only so much gold you can add to your portfolio before you start to look at yourself askance in the mirror. So they do nothing in a profound way. They don't increase risk but they don't diminish risk. They're averse to risk and they're averse to risk-aversion! It's a word without much meaning any more, and that's why I titled this note The Death of Risk.

It's a very weird place for an economy to find itself, where the entire idea of 'risk' gets obliterated because of an intentional erosion in the full faith and credit of the US government, and I think that all of our economic models and projections about what happens next are going to be wrong.

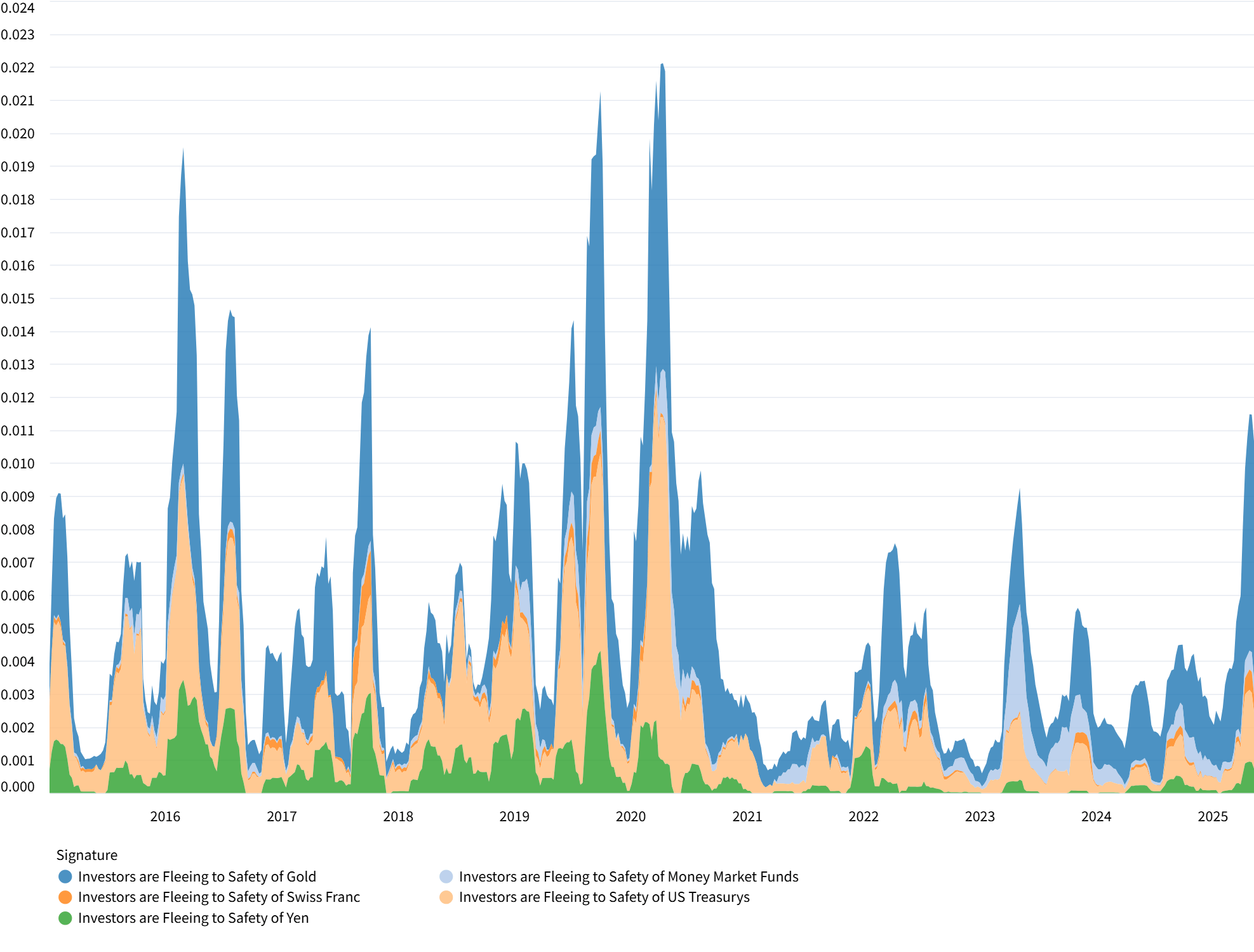

Let me show you just how weird a place we are in, where no one trusts the US government (or to a lesser and related sense the Japanese government) as a safe place to preserve their wealth when the world gets squirrely.

10-Year “Investors are Fleeing to X” Semantic Density (Raw Density)

This is a 10-year chart of the semantic density of investor narratives (what we call semantic signatures) concerning five "safety assets" -- gold, money market funds, US Treasuries, the Swiss franc and the Japanese yen -- across millions of financial news articles, blogs, research reports and transcripts. Semantic signatures are linguistic markers not for sentiment, topics, or keywords, but of a specific meaning that the author is trying to convey regardless of the specific words chosen to say it. Basically this technology gives us the ability to read everything in the world for meaning and then measure the mathematical density of that meaning-distribution across replicable linguistic structures. Lots of ten-dollar words in that last sentence, but if you want a more discursive introduction to the idea of semantic signatures please see The Four Horsemen of the Great Ravine, for a great brief note on the technology and the signals as shown through the topic of tariffs please see Narrative Shopping, and if you really want to dig into this we have an hour-long webinar Semantic Factorization Demo for Epsilon Theory Professional on our Professional site. All graphics shown here are from the Safety Asset Storyboard, one of six such semantic signature explorations also found on our Professional site.

What you're seeing in this chart is that whenever there's a market crisis or event that provokes risk-off and safe haven-seeking behavior, financial news media talks a lot about where that money is going. You see a lot of dark blue in that 10-year chart, which is gold, and you see a lot of tan in that chart, which are US Treasuries. Depending on the crisis, you see a fair amount of green, which is the Japanese yen. These are the go-to safety assets over the past ten years, especially gold and US Treasuries. The clear exception to this rule is our current risk-off, safe haven-seeking moment, where gold makes its usual appearance but US Treasuries and the Japanese yen are noticeably diminished from prior and similar risk-off moments.

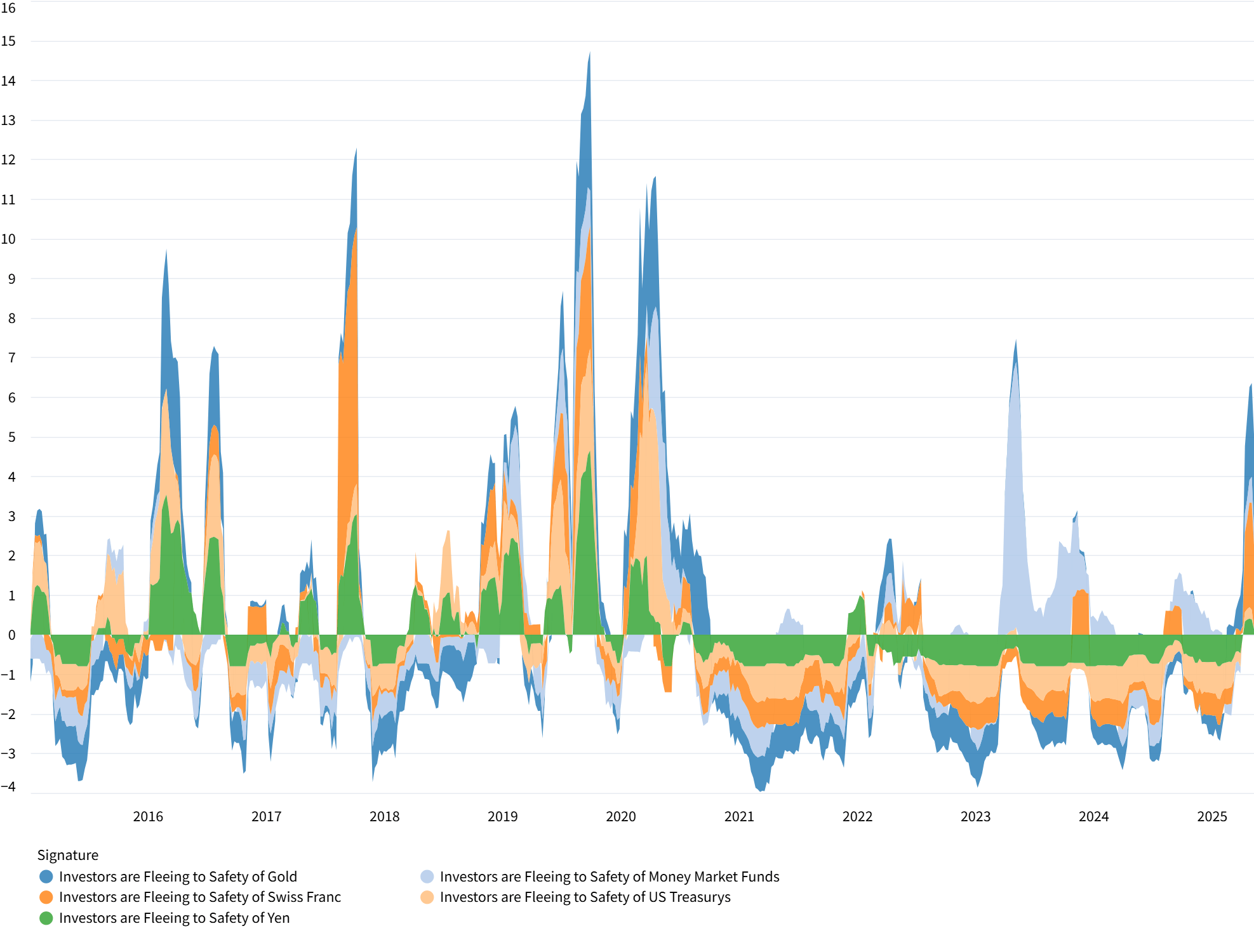

How diminished? Well, to answer that question, we can also represent the data as z-squared values, which is essentially a measure of how unusual (as expressed in standard deviations) a current 30-day linguistic density reading is from its average linguistic density reading. And that's the chart below.

10-Year “Investors are Fleeing to X” Semantic Density (Z-Scored)

Here it's a little more obvious that the tan (US Treasuries) and green (Japanese yen) semantic signatures are missing in action today, while the dark blue (gold) and orange (Swiss franc) semantic signatures are much more prominent today than usual. Separating these out and looking at the safety assets individually over time shows this phenomenon even more dramatically (I'm going to leave the Swiss franc out of this discussion because it's more of a Professional topic).

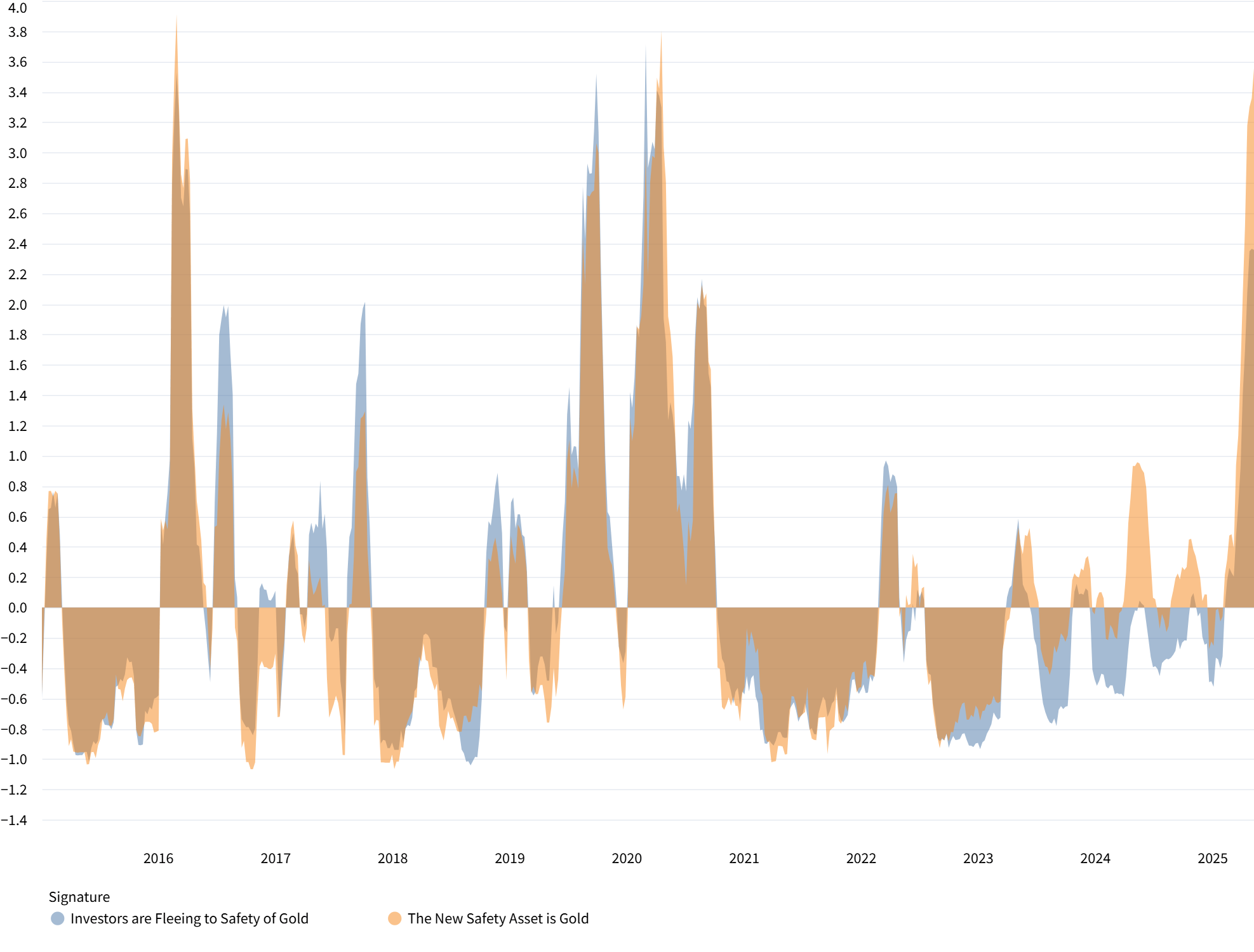

Let's start with gold.

10-Year Gold Safety Asset Semantic Density (Z-Scored)

We're showing here an overlay of both the "Investors are fleeing to safety of X" semantic signature as well as "The new safety asset is X" signature in these individual charts to demonstrate the robustness of these findings. However you formulate the story arc around gold as a safe haven, either as a existing safe haven or as a new alternative to other safe haven choices, the market narrative around gold is just as prominent today as it was around Covid or the first China trade war during Trump I. It was a big deal then and it's a big deal now. Gold is acting the way gold always acts.

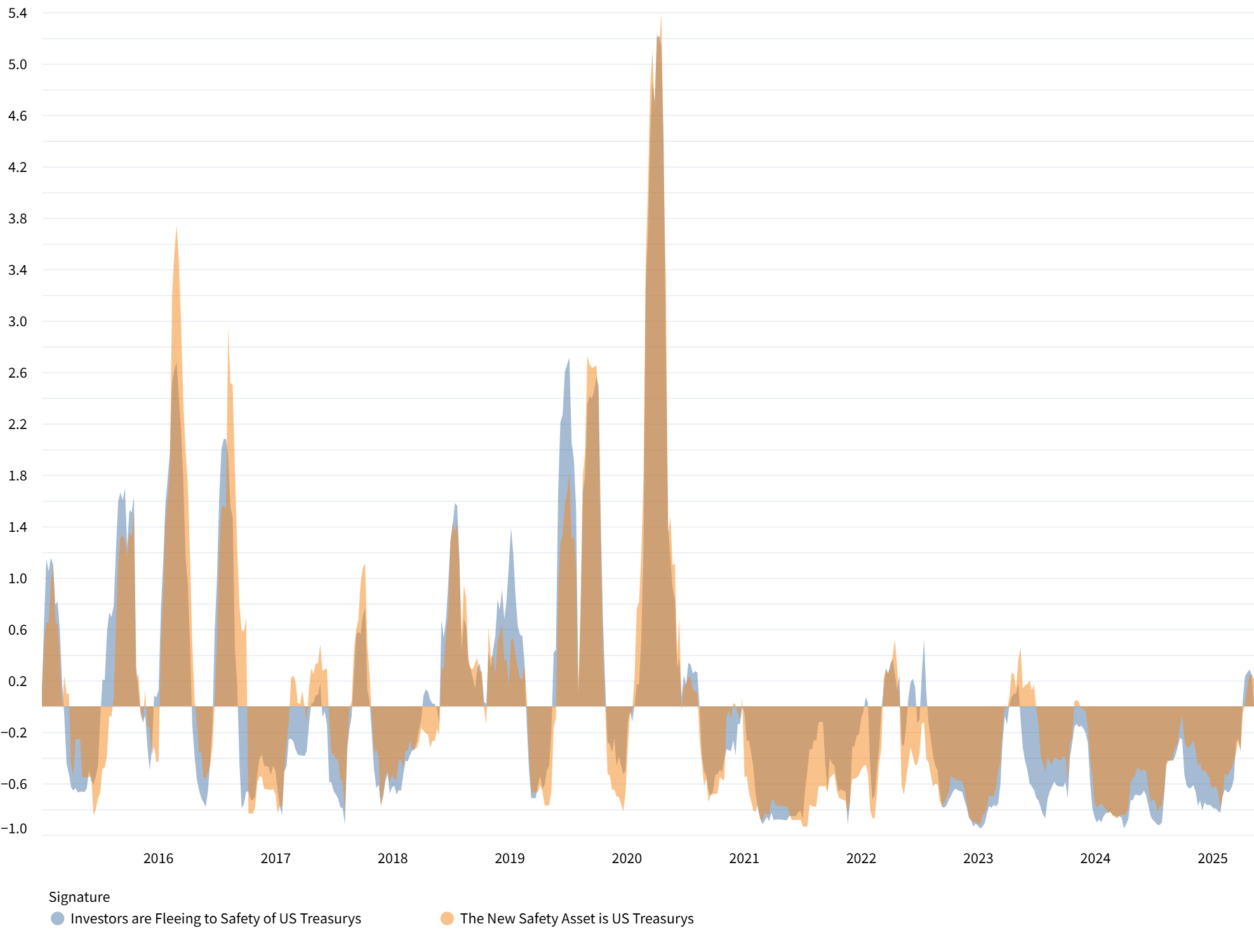

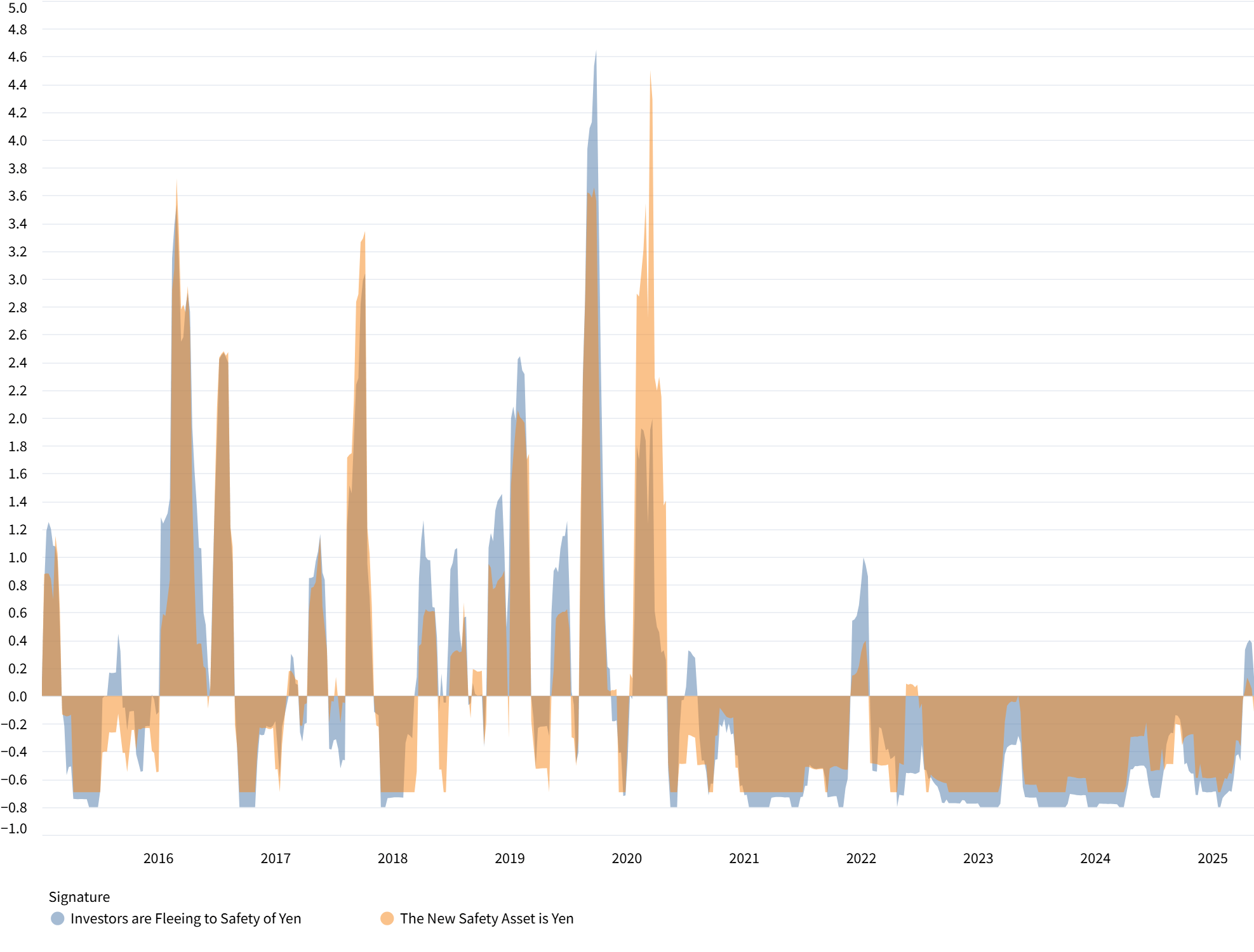

What's different today is the total absence of market narratives around US Treasuries and the Japanese yen as safety assets, as shown in the two charts below.

10-Year US Treasury Safety Asset Semantic Density (Z-Scored)

10-Year Japanese Yen Safety Asset Semantic Density (Z-Scored)

It's really pretty stunning how the largest sovereign bond market in the world (the United States) and the third largest sovereign bond market in the world (Japan) are now no-fly-zones when it comes to safe havens and risk-off behaviors.

No one thinks their money is safe in US Treasuries because no one trusts the chief executive of the United States to manage our country's debt any differently than he managed his casinos' junk bonds, cramming down bondholders when it suited him and otherwise using debt as a weapon rather than a promise. Relatedly, no one thinks their money is safe in Japanese yen because no one trusts the Bank of Japan to allow their currency to appreciate too far against the resulting US dollar weakness.

I think Jay Powell used some variation of the phrase "wait and see" about 200 times in his most recent press conference. He didn't sound particularly happy about it. But that's where every US investor is today, in an unhappy, profoundly do-nothing "wait and see" situation, where you don't completely trust the investment opportunities you're offered (anyone know how private credit as an asset class performs in a recession? what's that? you say there's no actual experience to draw from, just imputed experience from BB credits? great.) and you really don't trust the safe havens you've always used. As one insurance CIO told me the other week, "I feel reasonably fine about our risk portfolio; it's the risk-free portfolio that keeps me awake at night". Not that there's anything that this CIO can do about it. He can't hedge the risk-free portfolio of US Treasuries. Because it IS the hedge. So he just doesn't sleep.

Like I said, I'm still trying to figure out where this all goes, and all I'm confident in saying is that none of our macroeconomic growth/inflation models or our banking and insurance regulatory capital models or our portfolio diversification/allocation models work if the concept of risk loses its meaning. No biggie! But that's exactly what I think happened. I think the concept of risk is meaningless and dead if there's not a concept of non-risk to compare it to, and as much as I like gold as a concept of non-risk it's just not big enough to replace the US Treasury market.

The death of risk happened with a whimper, not a bang. It happened not because the market blew up in a fiery mess, but because of an icy truth that we all now know that we all now know: risk-free debt ain't risk-free. If you don't trust the meaning of risk-free, you can't trust the meaning of risk, and we have built everything on the meaning of risk.

It's not a market collapse that I see coming out of all this. That's fire. All I can see is the long gray slog of stagflation. And I think that's worse.